"96 fee change", what changed?

In March 2016, the National Development and Reform Commission and the Central Bank issued the “Notice on Improving the Pricing Mechanism for Bank Card Credit Card Fees†(hereinafter referred to as the “Noticeâ€), which made important adjustments to the charging model and pricing level of the bank card acquiring business. "It was officially implemented on September 6, 2016, so it was called "96 fee change" in the industry.

Before the fee change, the fee for the implementation of the bank card receipt business was the “Notice on Optimizing and Adjusting the Bank Card Fees†issued by the National Development and Reform Commission on January 16, 2013 (Development and Reform Price [2013] No. 66), the notice The merchant classification was adjusted from six categories to four categories, and the credit card fee standard was lowered overall, with an average reduction of approximately 24%.

The 96 fee reform continued the general tone of reducing the cost of the entity business, and made major changes in terms of “marketization pricing, separation of loans and cancellation of merchant categoriesâ€, and in some sense will reshape domestic bank card receipts. The competitive landscape of the market.

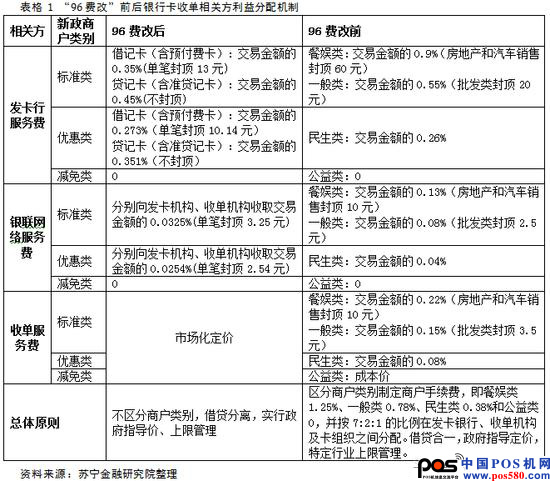

The following Table shows the changes in the fees charged by the parties involved in the bank card receipt market before and after the 96 fee change. Except for the unobligated rate level of the market-directed pricing from the government-guided price, the issuing bank and UnionPay rate levels appear. Different degrees of decline.

In addition to the intuitive rate reduction, the changes in the market operating principles proposed by the 96 fee reform will have a far-reaching impact on this market. The author analyzes it in three points.

Key point 1: The order of the acquisition is changed from government pricing to market pricing, ending the online and offline dual-track system.

Before the 96 fee reform, the nominal acquiring market implemented government pricing, but in reality it was a two-track system of “offline acquiring government pricing and online business market pricingâ€.

Under-line acquiring business, everyone is taking the channel of UnionPay, they must act in accordance with the rules of UnionPay, but the online payment business, third-party payment explores the direct bank connection mode, UnionPay becomes an outsider, 7:2:1 The interest distribution mechanism will cease to exist, and third-party payment companies will be able to bargain with the issuing bank and re-determine the fee allocation mechanism.

The online and offline price double track is a great driving force for channel adoption by some acquirers. On the one hand, it creates unfair competition in the industry and exacerbates bad money to drive out good money. On the other hand, channel application makes transaction data messages unable to restore business operations. The real scene brings huge hidden dangers for subsequent merchant management and risk prevention and control.

Although the fee reform has not directly proposed the abolition of the concept of online and offline dual-track system, the market-based pricing of the acquiring link has made the offline offline charging standard have the same space. The necessity of adopting the channel risk by violating the irregularity is naturally greatly reduced. It is.

Key point 2: Unified merchant category, consumption rate, echelon pricing

In recent years, the acquisition market has become more and more chaotic, and the violations such as set-ups and cutting machines have been repeatedly banned. The acquiring institutions have repeatedly “harvested†the central bank and UnionPay’s fines. Behind the code set is a huge difference in the handling fees of different merchants. The charge level for meals and entertainment is 1.25%, and the level for people's livelihood is 0.38%. For small merchants with 10 million waters a year, the package is set by the restaurant. People's livelihood can save 87,000 yuan, and the risk is very low (for merchants), why not do it.

The prevalence of the package also provides the soil for the cutting machine. In order to seize the merchants of the B acquiring institution, the A acquiring institution can win the support of the merchant by providing the package service, which in turn forces the B acquiring institution to take a step ahead. Proactively provide package services for its merchants.

Although the 96 fee reform still retains the three categories of standard, preferential and relief categories, it clearly requires that “the transition period from the formal implementation of this credit card adjustment measure will remain stable throughout the two-year transition period. In principle, the implementation of the card-issuing service fee and network service fee for supermarkets, large-scale warehouse stores, water and electricity gas payment, fueling, and transportation ticket merchants.

This means that after the two-year transition period, the merchant category will only have standard classes and reductions, basically unifying the merchant category, and the rate-based pricing method will naturally become history. At that time, the set code will lose the existing soil, and the cutting behavior will be greatly reduced.

.

Highly recommented

Use standard rate of 0.6% or more

First, the traditional pos machine: 0.6% (the lowest reasonable rate)

Second, mobile phone POS: 0.6% or more (100% of merchants below 0.6% have problems)

0.63% is generally reasonable: the profit is low, the expenses of the payment company and the agent are limited, and the merchants often jump to the field, public welfare, and reduction.

0.65% is more reasonable: the profit is general, the payment company and the agent are limited, and the merchant will occasionally jump to the field, public welfare, and exemption.

0.69% reasonable: the profit is enough to pay the expenses of the company and the agent, and the merchant is perfect.

Note: The questions about credit card withdrawal, derating, and sealing are here.

The fee for the credit card processing fee was adjusted after the 9.6th in 2016. And the proportion of the entire system has also changed. The original issuer, UnionPay, payment company, and the ratio of the three parties 7:1:2 have been broken. The original 1.25% and 0.78% rates have also disappeared.

The current rates are divided into three categories: standard class 0.6, deductible class 0.38-0.48, and public welfare class 0 rate.

Standard class: 0.6% rate

Reducing and exempting class: The issuing bank charges 0.325%, so the fee for the exemption class is generally 0.38%-0.48%.

Public welfare category: Public welfare category 0 rate

This shows that the payment company's cost rate is 0.4825. The payment company's rate space is 0.6-0.4825. But the operating costs of the payment company are relatively high. So if you see a POS machine with a rate of around 0.5, it is definitely a set of waivers or a 0 rate. The payment company must guarantee that the rate will be around 0.54 to maintain its own operation, and other handling fees should be extended to the agent. Therefore, the standard class fee is definitely 0.6 is the most reasonable.

There are still a lot of 0.6 seconds to the market, and even the credit card topper is how to do it?

Because the second to the funds are paid by the payment company in advance, the cost of advancement is between 0.05% and 0.1%. If the second is only 0.6%, if the bill is in the standard industry, the payment company must lose money, so 0.6 seconds to 100% of the product should be skipped or exempted.

There is also a credit card capping machine, which is definitely a 0 rate. In addition, there are still smart phones that look high-end. In fact, they are not used in the bank card collection system. The cost of the Internet is low, so it is not surprising that the credit card is capped.

There is an old saying in China, it’s really not cheap, and it’s not cheap! If you use low-rate POS machines again and again, will your card-issuing bank still let you use it? If you stare at it, it is easy to fall into the low rate trap. In the end, there is no guarantee of financial security. Credit card derating, sealing

Desk Table,Office Desks,Wood Computer Table,Office Computer Table

STARWAY INTERNATIONAL HOME-LIVING CO., LTD , https://www.starwayfurniture.com